Argentina - The Dollarization Debate

December 2023

Argentina - Mechanism and Risks of Dollarization

In November 2023 Argentina elected a new President, Javier Milei, who campaigned on promises of radical reform including dollarization of the Argentinian economy. For decades Argentina has been plagued by high inflation and in 2023 the inflation rate had exceeded 150% per annum causing living standards to plunge and investment to stall. The only recent decade during which Argentina experienced low inflation was during the 1990’s when it had a Currency Board which tied the Peso to the Dollar at a 1:1 rate.

Comparisons often help to illuminate a situation and one Latin American example, that springs to mind, of a country that pulled out of an inflation spiral to return to the path of growth is Peru in the 1990’s.

Peru

In 1980 Peru had inflation at 60% p.a. and interest on its external debt of $934m p.a. having borrowed in the 1970’s to fund purchases of Soviet arms.

In 1985 the elections were won by 36 year old Alan Garcia of APRA:

Interventionist State.

17 different exchange rates.

7 different rates of interest.

Price controls.

Payments on external debt were limited to 10% of export earnings - this unilateral measure meant that Peru was technically in default and cut-off from international credit markets.

Some of the effects of these policies were:

The collapse of Government revenues falling to below 9% of GDP in 1989 (a very ironic outcome for a statist politician)

Nationalization of banks

Hyperinflation (000's of % p.a.) when Garcia left office

Drastic fall in GDP by as much as a quarter following two years of growth when he first took office.

Fujimori, elected in 1990, adopted a return to financial orthodoxy and in his second year he had managed to get the State deficit down to the 3-4% of GDP range where it was manageable. He also succeeded in getting inflation down, though more gradually over the course of the decade, to low single digits. Growth in his first five years in office was patchy and often negative but was much better in the second five years as the effects of sound policies began to be felt. Fujimori effectively followed IMF shock therapy.

The results can be seen on the charts below:

A large contraction during the latter part of Alan Garcia’s term of office

Slow recovery under Fujimori followed by a rebound in 1994 and then growth settling into a pattern of 5% per annum on average

This average rate of growth continued into the Millennium except for the Covid dip in 2020

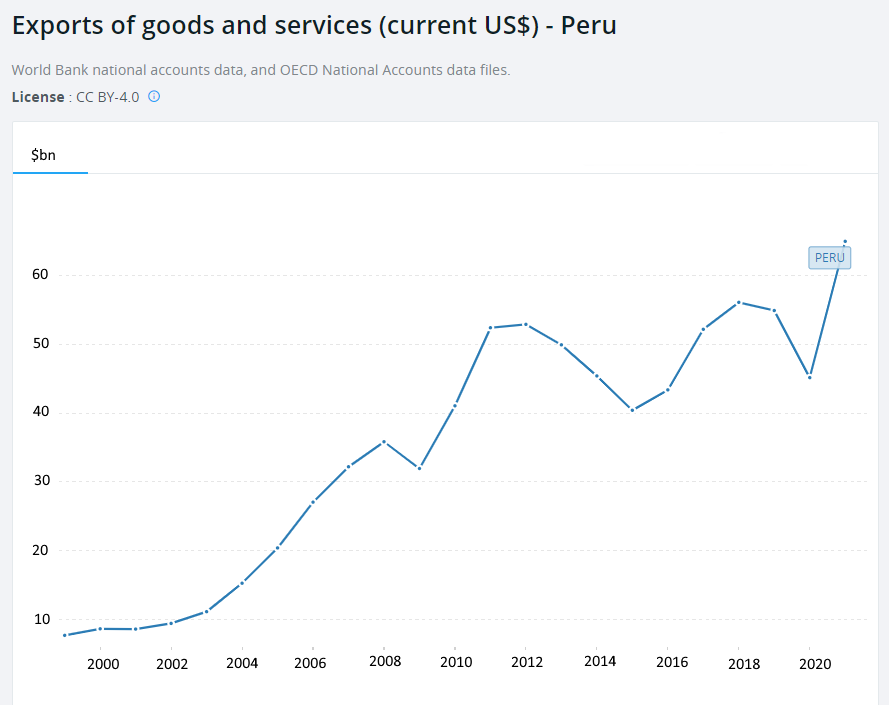

Exports have grown continuously from a low base and China is the largest export market. Exports are overwhelming primary products with copper representing the largest single export product.

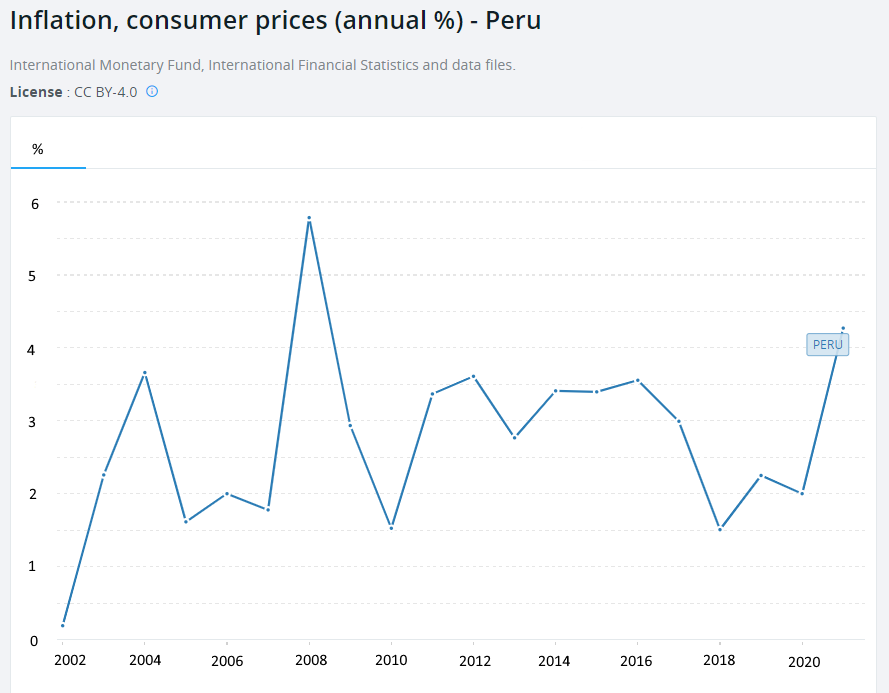

Inflation has been tamed, averaging about 3% a year

Low inflation is consistent with orthodox fiscal policies where public spending is kept under control

Peru uses its own currency, the Sol, which has lost about 6% of its value against the US$ since the Millennium (23 years)

Peru was transformed from a basket case in 1990 into a candidate country for OECD membership in 2022.

Argentina

Inflation is not quite so severe in Argentina as when Fujimori took office in Peru in 1990 and exports are considerably higher in relation to the economy but the other problem of unbudgeted fiscal deficits causing inflation and a lack of confidence is present.

Peru shows that dollarization is not a precondition of a successful turn-around. The main issue is to bring the public finances under control in order to get inflation down and then to promote export growth and investment.

However, Argentinians have long shown a propensity for transferring money out of the country and this tendency is likely to persist even if they succeed in getting inflation down. Money held by Argentinians in other currencies, e.g. US$, crypto etc, is still part of the economy in that it is part of their wealth and affects their spending decisions.

Transfers out of Pesos into Dollars and other currencies are subject to a tax known as the Cepo. When Mauricio Macri became President in 2015 his first act was to abolish the Cepo and in my view this was the ruin of his Presidency as Argentinians rushed to exchange their Pesos for Dollars and the resulting outflow caused the demonetization of the economy and a foreign exchange crisis.

What the Milei Administration needs to do is:

Fix the budget deficit by reducing spending

Grow exports to generate trade surpluses

Once the Government finances are in order measures can be taken to reduce inflation

The exchange rate should adjust to reflect higher internal inflation than the international rate

If they want to dollarize the economy they are going to need to access the pool of dollars held abroad so they would need to devise a mechanism where that could flow back naturally. Lifting the Cepo (foreign exchange tax) will only encourage more money to leave the economy.

Argentina has 10 million crypto users or about 1/3 of the adult population.

Is possible to dollarize gradually? In many developing countries contracts between companies are often written in US Dollars but then settled in the local currency. This is to protect buyer and seller from a drop in the value of the local currency. In Argentina it could be possible to take this practice a step further and require actual settlement in Dollars. This would be feasible because of the large Dollar holdings abroad of Argentinians such that this requirement ought not to cause liquidity problems in the economy.

If we look at Argentina’s net international reserve position end Q2 2023 on the table below we have

A large Government net liability of US$98bn

Direct Investment shows inward investment exceeds outward investment by US$83bn – this is not, in itself, a negative outcome since it reflects overseas companies investing in the Argentinian mining, oil and other sectors

A surplus of portfolio investment of US$65bn

A surplus of other investment (e.g. overseas deposits etc) of US$213bn

Portfolio and Other Investments have a combined surplus of US$278bn and Government has a net liability of US$98bn indicating a substantial net asset position for Argentina. There are also, of course, significant unrecorded assets in cash, crypto, gold and other valuables.

Were Argentina to partially dollarize by requiring e.g. corporate investment transactions, property transactions and large individual purchases to be completed in Dollars then this would allow the Government, and hence the Central Bank, to gradually build up its holdings in Dollars as these transactions are subject to tax. The day to day economy could remain in pesos for the time being.

Cash in circulation is usually a small percentage of GDP – see the table below.

Inflation in Pesos will fall when the Government gets its own finances under control and thus, like Fujimori in Peru in the 1990’s, this means taking an axe to Government spending in the short term.

Concluding Remarks

Peru managed to find a way out its inflation spiral by adopting fiscal orthodoxy and without dollarizing. However, Argentina is different and I don’t see how it is possible to move forward without co-opting the vast overseas Dollar holdings of the Argentinian population. This could be achieved by requiring settlement in Dollars and allowing the State to build up its own Dollar holdings.

In Argentina LETIQS (Letras de Liquidez) are short term Treasury Bills held by Banks and these have interest rates which follow the inflation rate; i.e. they are very high and cost the Argentinian Treasury a vast sum which affects its budgetary finances. If these were rolled over to Dollars as they were redeemed then the interest rate payable would fall to the international rate and this measure, in itself, would have a significant effect on the Government finances. Lower interest rates would then allow private sector investment to resume.

If Argentina does go the Dollar route then if it converts at market rates its exports will be competitive and it won’t run into the roadblock with the Currency Board of the 1990’s where the exchange rate of the Peso to the Dollar was too high. Another question is the US Dollar itself; it is possible that this will become unstable in the coming years unless the US gets its deficits under control. In such a scenario Argentina could switch to another currency such as the Euro or the Yuan by converting its Dollar holdings.

Javier Milei is somewhat of a maverick figure whereas Alberto Fujimori was the staid professorial type. However, following his first two terms during which he restored confidence in the Peruvian economy, Fujimori did something highly unconventional (for which he has spent more than a decade in jail). After having secured a third Presidential term he absconded to Japan, where he had a second citizenship, leaving Peru in constitutional limbo and took with him a significant sum of money from the Peruvian Treasury. Thus, it would be better to judge Milei on his achievements rather than the image he projects.

Milei won the Argentinian Presidency as a protest vote as a majority recognize that something has to change. In my view, the dollarization route is the correct one in the short term if it is executed correctly. It would allow inflation to return to low single digits, interest rates to fall in tandem and investment to resume.